Climate Action Framework

The challenge of meeting the world’s growing need for energy while simultaneously ushering in a lower-carbon future is massive, intertwined and fundamental. It is the opportunity of our time – governments, industries, and consumers must rise to seize it together.

PDFs: API Climate Action Framework - Executive Report

Optical gas imaging cameras, a specialized version of an infrared or thermal imaging camera, are used across the natural gas and oil industry to detect methane emissions and identify leaks for timely repair.

The United Nations has projected that global population will increase from 7.7 billion in 2019 to nearly 10 billion in 2050, and energy demand will grow with it – and grow the fastest among many emerging economies that struggle today to alleviate energy poverty. The world needs solutions that advance human and economic development, enable emerging economies to progress while also developing their own domestic resources and satisfy global energy needs in ways that are compatible with reducing greenhouse gas emissions and achieving environmental progress.

Jump to Climate Actions:

The International Energy Agency (IEA) projects demand will return to pre-COVID levels in early 2023 and increase nearly 10% by 2030, led by demand from developing economies. Official estimates from the U.S. Energy Information Administration (EIA) project even greater global energy demand growth in a scenario where energy policies remain relatively steady. Energy demand is likely to continue to grow against the backdrop of humankind’s quest for a lowercarbon future – in which energy production, transportation and use are aligned with global climate objectives.

Our industry is at the center of this challenge. Natural gas and oil provide more of the world’s energy than any other source and will continue to be leading resources for decades to come.

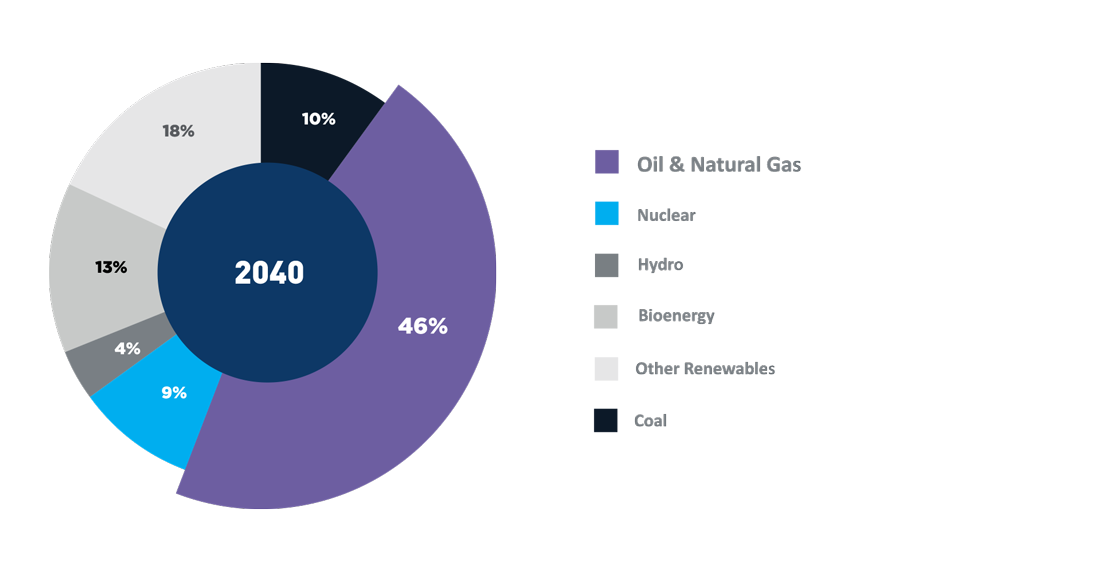

World Energy in 2040: Natural Gas and Oil Will Continue to Lead

Under the IEA’s Sustainable Development Scenario, natural gas and oil will furnish nearly half the world’s energy in 2040, even if every nation meets the goals of the Paris Climate Agreement.

Our industry is essential to supplying energy that makes life modern, healthier and better – while doing so in ways that tackle the climate challenge: lowering emissions, increasing efficiency, advancing technological innovation, building modern infrastructure and more.

This framework lays out what government can do, what our industry will do and what policies will enable our continued efforts to ensure energy delivery and emissions reduction. We will continue innovating to further reduce production-related emissions and to make delivery systems and consumer products that achieve environmental progress. We will build on our industry’s long history of developing technologies and solutions that advance modern life.

We will support carbon pricing mechanisms that work across the entire economy to maximize environmental benefits.

We will increase transparency so that our progress is understandable by all.

And we will partner with government on these and more, while encouraging policymakers to recognize the nation’s need for more energy and the infrastructure to safely transport it to consumers.

We support further innovation, new economywide market mechanisms and sensible policy proposals to enable a better tomorrow. Through the following actions and beyond, API member companies will work toward a cleaner energy future together with government partners, other industries and fellow innovators.

API's Climate Framework

We share with global leaders the goal of reduced emissions across the broader economy and, specifically, those from energy production, transportation and use by society. To achieve meaningful emissions reductions that meet the climate challenge, it will take a combination of policies, innovation, industry initiatives and a partnership of government and economic sectors. The objective is large enough that no single approach can achieve it.

Industry Action Plan:

- Accelerate Technology and Innovation to reduce emissions while meeting growing energy needs

- Advocate for Federal Funding for Low-Carbon RD&D

- Fast-track the Commercial Deployment of Carbon Capture, Utilization and Storage (CCUS)

- Advance Hydrogen Technology, Innovation, and Infrastructure

- Further Mitigate Emissions from Operations to advance additional environmental progress

- Advance Direct Regulation of Methane from New and Existing Sources

- Develop Methane Detection Technologies

- Promote Reductions in Refinery GHG Emissions and Mitigate Upstream Flaring Emissions

- Endorse a Carbon Price Policy by government to drive economywide, market-based solutions

- Potential Approach Would Price Carbon Dioxide Emissions Across the Economy

- Support Policies that Provide Transparency for Consumers

- Minimize Duplicative Regulations and Help Maintain U.S. Competitiveness

- Avoid Carbon Leakage and Integrate with Global Carbon Markets, while Focusing on Net Emissions

- Advance Cleaner Fuels to provide lower-carbon choices for consumers

- Develop Markets for Differentiated U.S. Natural Gas

- Support Policies to Advance Lower-Carbon Electricity

- Reduce Lifecycle Emissions in the Transportation Sector

- Drive Climate Reporting to provide consistency and transparency

- Expand Use of ESG Reporting Guidance for the Natural Gas & Oil Industry

- Report Comparable Climate-Related Indicators in New Template

- Build on the API Compendium of Greenhouse Gas Emissions Methodologies for the Natural Gas and Oil Industry

Accelerate Technology and Innovation

Our industry’s focus is on technologies that have shown they can reach the largest commercial scale and maximize emissions reductions in ways that are cost-effective for the industry and consumers.

Advocate for Federal Funding for Low-Carbon RD&D:

Deploying low-carbon technologies can meaningfully reduce emissions while delivering essential energy. API members support innovative partnerships and technological development and deployment. For example, carbon capture, utilization, and storage (CCUS) – taking carbon dioxide (CO2) emissions from facilities and storing and/or repurposing them – is key to cleaner energy use across the economy. This technology is advanced by the 45Q tax credit, providing support for CCUS deployment, and by increased federal research and development funding, which was a focus in recent federal legislation. API is pushing for full federal funding of research, development and deployment (RD&D) programs, authorized in the bipartisan Energy Act of 2020. These are viable ways to reduce greenhouse gas (GHG) emissions from energy-intensive industries. API also supports significant increases in congressional funding of government research on a range of low- or zero-carbon technologies, including CCUS and hydrogen fuel development. Funded technologies should show the greatest potential for reducing GHG emissions at the lowest possible cost to the economy.

Fast-track the Commercial Deployment of Carbon Capture, Utilization and Storage (CCUS):

The United States is the world leader in deploying CCUS technology. The U.S. has 12 commercial-scale, operating CCUS facilities, capable of capturing approximately 25 million metric tons (MMT) of CO2 annually. In 2018, operators reported capturing more than 13 MMT of CO2 for use with enhanced oil recovery. An additional 22 U.S. carbon capture facilities are being developed. Many are associated with natural gas power generation, though natural gas and oil firms are also partnering with other industrial firms to expand CCUS in heavy industry. API supports federal policies to achieve the “at-scale phase” of CCUS commercial deployment, consistent with the 2019 findings of the National Petroleum Council. This includes extending and expanding the 45Q tax credit and permitting reforms to streamline CO2 infrastructure development.

U.S. Carbon Capture Facilities (Operating and Under Development)

Carbon Capture Capacity

Source: GCCSI, Global Status of CCS, 2020

The U.S. leads the world in deploying CCUS technology. Commercial-scale facilities can capture about 25 million metric tons

of CO2 annually.

Advance Hydrogen Technology, Innovation, and Infrastructure:

Hydrogen is increasingly recognized as a valuable pathway for meeting ambitious climate goals – particularly in reducing emissions from hard-to-abate sectors. Expanding the role of hydrogen in decarbonization requires cost-effective production of low-carbon hydrogen from all sources. Today, most hydrogen is produced with natural gas, which, if paired with CCUS, offers a promising and scalable low-carbon fuel source.

API supports policies that advance the technology-neutral development of low-carbon hydrogen and the use of hydrogen in carbon-reduction efforts.

API will also advocate for and support policies that advance hydrogen infrastructure buildout – a critical and necessary component of expanding hydrogen demand. Based on the natural gas and oil industry’s research abilities and expertise, we can help further advocate for the development and promotion of promising hydrogen technologies.

Carbon Intensity of Hydrogen Production

Source: The Future of Hydrogen. International Energy Agency. 2019

Hydrogen derived from natural gas in conjunction with CCUS technology, such as blue hydrogen, offers scalable, low-carbon

hydrogen production.

Further Mitigate Emissions from Operations

API member companies support reducing emissions from operations in the following ways:

Advance Direct Regulation of Methane from New and Existing Sources:

Reducing methane emissions is a priority for our industry to address the risks of climate change. Methane emissions account for approximately 10% of total U.S. GHG emissions on a CO2-equivalent basis, according to EPA. Among methane sources, EPA finds natural gas and oil production, processing and transmission contribute approximately one-third of U.S. human-caused emissions. As a result of technology and efficiency measures, emissions relative to production in the largest producing basins were down nearly 70% between 2011 and 2018 and continue to trend downward.

Falling Methane Rates in Natural Gas Production from Key Basins

Methane emissions per unit of production from key basins fell nearly 70% between 2011 and 2019, indicating industry’s increased efficiency in reducing emissions, according to data from EPA and EIA.

We support cost-effective policies and direct regulation that achieve methane emission reductions from new and existing sources across the supply chain.

The Environmental Partnership is comprised of 90 upstream and midstream companies in the U.S. natural gas and oil industry working to continuously improve the industry’s environmental performance.

Implemented in 17 of 21 top-producing states, membership has more than tripled since the program’s 2017 launch.

Nineteen of the top 20 U.S. natural gas producers are participating companies.

2019 Results:

- Increasing Leak Detection and Repair:

- More than 87,000 sites surveyed

- More than 116 million component inspections performed

- More than 184,000 surveys conducted

- 0.08% leak occurrence rate, or less than 1 component leaking in 1,000

- Prioritizing Better Equipment:

- More than 10,500 additional gas driven controllers replaced or removed from service

- More than 3,300 high-bleed pneumatic controllers replaced, retrofitted, or removed from service

- More than 2,800 zero-emission pneumatic controllers installed at new sites

- 43 participating companies no longer have high-bleed pneumatic controllers in their operations

- Improving the Manual Liquids Unloading Process:

- Emissions minimized by monitoring more than 44,000 manual liquids unloading events

Additionally, our industry remains devoted to the development and deployment of new technologies and practices through industry initiatives such as The Environmental Partnership to better understand, detect and mitigate emissions.

Develop Methane Detection Technologies:

The natural gas and oil industry is committed to advance the development, testing, and utilization of new technologies and practices to better understand, detect, and further mitigate emissions.

Promote Reductions in Refinery GHG Emissions:

Individual refineries are working to reduce GHG emissions and drive energy efficiencies. Many refiners also provide data to third parties on their energy efficiency and carbon-emissions intensity to track performance and identify opportunities for improvements. API will engage in the evaluation of a coordinated refinery carbon-emissions reduction program to reduce GHG emissions. This program will identify an achievable target that will result in meaningful GHG emissions reductions. Participating companies will report their performance to API annually through a third-party organization, and API will conduct industry forums to share information on topics such as refinery carbon reduction and overall energy efficiency. The forums will protect company intellectual property and conform to API antitrust guidelines.

Mitigate Upstream Flaring Emissions:

Energy producers have reduced emissions associated with flaring – voluntarily and under federal and state regulations. Industry can further improve current practices and reduce GHG emissions while also minimizing natural resource loss from flaring of associated gas that occurs during production.

To reduce emissions associated with flaring, operators are increasingly aligning production, gas-gathering and processing infrastructure to provide environmental benefits and conserve resources. They are identifying alternative beneficial uses of the associated gas to prevent flaring where gas-gathering infrastructure is unavailable.

API supports company efforts toward no routine flaring by a date certain, for example the World Bank’s Zero Flaring Initiative by 2030.

Our goal is to better understand and ultimately inform the discussion of goals for reducing economywide associated-gas flaring.

The Environmental Partnership already includes a flaring management program that focuses on companies sharing information on best practices, advancing new and proven technologies, fostering collaboration to reduce emissions and collecting data to guide efforts to minimize flaring. API is developing an operational guide on flaring, based on best practices identified by The Environmental Partnership.

In addition, API developed Standard 537, Flare Details for Petroleum, Petrochemical, and Natural Gas Industries, which provides guidance and good engineering practices for the selection, design, operation and maintenance of flares, and is applicable across the natural gas and oil industry. The standard incorporates the newest technology for combustion equipment to improve design and operation of the flaring processes, ultimately helping to reduce flaring and decrease CO2 emissions.

The Environmental Partnership’s Flaring Management Program – launched in 2020 – applies to high-pressure flaring of associated gas at onshore production, gathering, and boosting oil field sites. In specific instances, flaring is safer environmentally than venting gas to the air. Flaring releases fewer GHG emissions than venting. Under the program, participants:

- Advance best practices to reduce flare volumes

- Promote the beneficial use of associated gas

- Improve flare reliability and efficiency

- Collect data to calculate flare intensity

- Report actions taken that The Partnership will aggregate annually

Endorse a Carbon Price Policy

Rather than a patchwork of federal and state regulations and mandates that could ineffectively address the climate challenge, an economywide government carbon price policy is the most impactful and transparent way to achieve meaningful progress. We recognize there are different ways for policymakers to consider carbon pricing – from a cap-and-trade system to a carbon tax – but there are some general parameters to begin the discussion.

Policy should be:

- Economywide: API will engage policymakers so that the design of a potential approach would price carbon at the outset for all relevant GHG emissions across the economy, from all relevant sectors and all emitters, accounting accurately for the benefits, costs and amounts of GHG emissions. Policies should support significant investments in innovation to develop technologies that lower the cost of GHG emissions abatement across the economy. Policy should be based on carbon-equivalent emissions on a common unit and time period of measurement (i.e., GWP100) basis across the U.S. economy, as practically and economically achievable as possible.

- Transparent: The carbon pricing system should be designed so that consumers have transparent incentives, based on actual GHG emissions if possible, to reduce GHG emissions efficiently. With respect to transportation fuels, a government policy-imposed carbon price should be disclosed at the point of retail sale. To provide certainty for the economy and maintain the integrity of the policy, the price on carbon or emissions cap should be adjusted periodically through a defined, rational and transparent process to meet GHG emissions targets. As applicable, the year 2005 should be the baseline against which future targets for reducing GHG emissions are determined. This already is the baseline for which U.S. economywide policy action has been determined in global climate negotiations.

- Nonduplicative: Policies should minimize the burden of duplicative regulations and be designed for a uniform cost of GHG emissions on a CO2-equivalent basis throughout the economy that does not exceed the marginal cost of carbon emissions abatement or the cost associated by an additional ton of carbon emitted into the atmosphere.

- Maintain U.S. Competitiveness: The goal of a carbon price policy should be to achieve GHG emissions reductions at the least cost to society, to meet the dual challenge of continued U.S. economic growth and global competitiveness while addressing the risks of climate change.

- Avoid Carbon Leakage, Integrate with Global Carbon Markets: Policy should be globally integrated, including through trade mechanisms, so that U.S. entities have the incentive to reduce their carbon footprint on a worldwide basis without being competitively disadvantaged and to avoid carbon leakage.

- Focus on Net Emissions: Attention should be given to net GHG emissions such that ongoing voluntary actions are recognized and the trading and use of applicable credits and offsets is allowed.

Advance Cleaner Fuels

The natural gas and oil industry is advancing cleaner fuels to provide consumers with lower-carbon options.

Our abundant supply of natural gas already has helped the U.S. achieve meaningful emissions reductions and will continue into the future. Over the past decade, electricity generation has been the primary source of demand growth for domestically produced natural gas. According to the EIA, natural gas demand in the power sector increased more than 110% between 2007 and 2019, and natural gas is now by far the largest source of power generation in the U.S., responsible for nearly 40% of total generation in 2020.

The concurrent fuel-switching from coal to natural gas in the power sector has been the leading driver of emissions reductions in the United States, a trend further aided by a significant increase in deployment of wind and solar. The continued availability of low-cost U.S. natural gas combined with a strong export policy – especially as it pertains to liquefied natural gas (LNG) – presents an opportunity to achieve continued success in emissions reductions around the world. According to the IEA, in 2018, coal to gas switching avoided 95 megatons of CO2 emissions globally.

In transportation, today’s automobiles are 99% cleaner than they were in 1970, and modern internal combustion engine vehicles help reduce real-world emissions per mile traveled on a fleet average basis.

Emissions from vehicles have reduced significantly due to cleaner fuels and advancements in their engines.

Emissions from passenger cars and light-duty trucks, accounting for most transportation-sector emissions, made up only 16.1% of U.S. GHG emissions in 2018. Real-world CO2 emissions per mile traveled for new light-duty vehicles have declined 48% since the 1975 model year.

Real-World CO2 Emission Rate for New Light-Duty Vehicles in the U.S.

Source: 2020 EPA Automotive Trends Report.

Vehicle emissions have fallen due to cleaner fuels and engine technology advancements.

Real-world CO2 emissions per mile traveled have declined 48% since 1975.

API proposes to advance cleaner fuels in three key areas: natural gas, electricity, and transportation.

Develop Markets for Differentiated U.S. Natural Gas:

API supports policies that expand the use of U.S. natural gas in both domestic and global markets – and for good reason. U.S. CO2 levels are at generational lows, due in large part to coal-to-natural gas switching in the power sector. According to the IEA, no other nation has reduced carbon dioxide emissions more than the U.S. since 2000. Today, natural gas serves as America’s leading fuel for electricity – used to meet nearly 40% of electricity demand – because it is a flexible, affordable, reliable and cleaner fuel for power generation. The unique attributes of natural gas are driving up demand around the world, and U.S. emergence as a major natural gas exporter has been key to meeting this demand. As investors and large natural gas customers of all types increasingly learn the emissions impact of their suppliers, there has been rising interest in a standardized and transparent market for natural gas classified by its emissions intensity (such as “differentiated” natural gas).

API supports the ongoing development of markets for “differentiated” natural gas, recognizing the significance of these efforts in ensuring that natural gas continues to play a critical role in a lower-carbon energy future.

API can use its expertise in developing industry standards to help promote transparency, credibility, and international recognition of differentiated natural gas from the U.S. Further, API Global Industry Services, the leading natural gas and oil industry standard-setter worldwide, can evaluate establishing criteria and methodologies for advancing differentiated natural gas.

Support Policies to Advance Lower-Carbon Electricity:

API endorses an economywide price on carbon, the most impactful policy for emissions reductions, but recognizes the prevalence of ongoing discussions regarding sector-specific policies, including a Clean Energy Standard (CES) focused on the electricity sector. API supports fuel- and technology neutral approaches to addressing emissions in the electricity sector and believes that any CES under consideration should include natural gas and recognize and value the many benefits natural gas provides to an increasingly lower-carbon electricity grid.

Reduce Lifecycle Emissions in the Transportation Sector:

API supports technology-neutral policies at the federal level that drive GHG emissions reductions in the transportation sector, taking a holistic approach to fuels, vehicles, and infrastructure systems. Policies under discussion include federal fuel standards, a full lifecycle approach to vehicle standards, optimization of fuel/vehicle systems to improve efficiency and supportive infrastructure measures.

Drive Climate Reporting

API supports timely and accurate reporting of GHG emissions from all emitting sectors in the economy to provide a transparent fact base for market-based solutions and government policy.

Policymakers, investors, other financial stakeholders and other parties require common understanding of the climate-related financial risks and opportunities of companies across the entire natural gas and oil value chain. To that end, API will promote the development of industry reporting on emissions in a transparent manner and leverage existing frameworks. In all our efforts in this space, we aim to enhance consistency and comparability in GHG reporting.

Here are some reporting initiatives already in place or in progress:

Expand Use of ESG Reporting Guidance for the Natural Gas and Oil Industry:

With its partners – the International Petroleum Industry Environmental Conservation Association (IPIECA) and the International Association of Oil & Gas Producers (IOGP) – API in 2020 updated sector-wide guidance for sustainability reporting, providing companies a common framework for assessing environmental, social, and governance (ESG) issues.

Report Comparable Climate-Related Indicators in New Template:

Our goal is to develop a concise minimum template of core GHG indicators, providing relevant information and enhancing consistency and comparability in reporting. An API template – developed in coordination with our membership – will help guide individual companies in their reporting.

Build on the API Compendium of Greenhouse Gas Emissions Methodologies for the Natural Gas and Oil Industry:

API’s Compendium of Greenhouse Gas Emissions Methodologies for the Natural Gas and Oil Industry serves as a key resource for companies’ timely and accurate estimation and reporting of greenhouse gas (GHG) emissions. The new edition of the Compendium, the first update since 2009, details methodologies for natural gas and oil industry segments to consistently estimate direct GHG emissions over the entire value chain. The work reflects the evolution of GHG calculation and incorporates what has been learned in this field over the past 12 years. For the first time, the Compendium includes expanded methodologies for liquefied natural gas (LNG), as well as carbon capture, use, and storage (CCUS).

Conclusion

Meeting growing energy demand will require investments, innovations, breakthroughs and a coalescence of the global community like we have never before seen. Our industry is prepared to tackle these challenges, lead where we are best positioned to develop solutions and work with policymakers, other industries and communities to supply the energy the world needs while working to reach the ambitions of the Paris Climate Agreement.

It begins here at home, and we need policy proposals in Washington, D.C. and around the country that support and advance affordable and reliable American energy while also reducing emissions.

The framework that API has outlined will make meaningful progress toward growing our economy, strengthening U.S. energy security and protecting the environment, while also enhancing U.S. energy leadership and the integral roles of natural gas and oil in the decades to come.

Downloads

API Climate Action Framework

API Climate Action Framework - Executive Report